While commercial leasing activity is anticipated to increase in 2024, it is also expected to linger below pre-pandemic levels, according to a recent survey by CBRE.

Read More

While commercial leasing activity is anticipated to increase in 2024, it is also expected to linger below pre-pandemic levels, according to a recent survey by CBRE.

Woodbridge, N.J. –April 11, 2024 – Visual Lease (VL), the #1 lease optimization software provider, today announced its Q1 results, reporting sustained double-digit annual recurring revenue and customer percentage growth,…

It took Gary Gensler’s SEC two years to get a rule requiring companies to disclose their climate impacts approved, but it’s only taken days for opponents to file legal challenges.

It’s clear that the journey towards and beyond compliance with lease accounting standards (ASC 842, IFRS 16, & GASB 87) is fraught with challenges and opportunities. The strategic importance of…

Businesses have encountered unique opportunities to transform their lease portfolios from mere contractual obligations into dynamic, strategic assets. This evolution, spurred by effective management and the integration of cutting-edge technology,…

The newly passed greenhouse gas disclosure rule from the Securities and Exchange Commission will have a significant impact on many industries, including commercial real estate.

The US Securities and Exchange Commission (SEC) approved its anticipated climate disclosure rules but watered down emission disclosure requirements under pressure from politicians and lobbying groups, making it less stringent…

The US Securities and Exchange Commission (SEC) has adopted its watered down climate risk disclosure rule in a disputed 3-2 vote, but its future remains uncertain in the face of…

The US Securities and Exchange Commission (SEC) has adopted the long-awaited rule to enhance and standardise climate-related disclosures, with multiple changes compared to the original draft – something that SEC…

After a long meeting, the SEC in a divided vote passed its long-expected greenhouse gas disclosure rule. While it changed “quite significantly” from the original more extensive form, as Anna…

The Securities and Exchange Commission voted 3-2 Wednesday morning to approve rules that would initially require large corporations to report part of their carbon emissions, but not Scope 3 emissions.

As businesses navigate the complexities of the post-pandemic landscape, the question of whether to lease or buy equipment is more pertinent than ever. The global health crisis, followed by economic…

A divided Securities and Exchange Commission voted three to two Wednesday to approve a new rule that would require companies to provide climate-related disclosures to investors, but scaled back the…

In the complex accounting landscape, fund accounting is a specialized area that demands meticulous attention, especially for non-profits, universities, hospitals, and governmental entities. Fund accounting is essential for these organizations,…

This guide shares what you need to know to understand different components of a lease, and how to be better informed to negotiate ideal lease terms to create additional financial…

In this blog post, we will provide a comprehensive breakdown of GASB 87 and explain what you need to know. Revisiting the Introduction of GASB 87 The lease accounting standard,…

ESG (environmental, social and governance) reporting has evolved into an essential cornerstone of corporate well-being due to its influence on critical stakeholders.

Best Practices for Negotiating Ideal Lease Terms We’re diving into the intricacies of GASB 96, a significant standard that government entities need to adopt, especially following the implementation of GASB…

We’re diving into the intricacies of GASB 96, a significant standard that government entities need to adopt, especially following the implementation of GASB 87. The Essence of GASB 96 GASB…

In our latest blog post, we delve into the findings of our Visual Lease Data Institute (VLDI) research that sheds light on the evolving terrain of lease accounting. About the…

We’re delving into the complex world of lease accounting and its tax implications, particularly in the wake of the COVID-19 pandemic. We’ll share valuable insights into how businesses, especially retailers,…

Lease accounting compliance isn’t a one-and-done disclosure, it’s an entirely new approach to accounting and an ongoing process. To make ongoing operations, reporting and compliance sustainable, you need controls that…

As the fiscal year ends, finance departments are undertaking the detailed process of year-end closing. This task demands intense focus on financial specifics and collaborative efforts across various functions to…

Adopting the ASC 842 lease accounting standard has been one of the most impactful changes in accounting practices, particularly for private companies gearing up for compliance. Drawing from the experience…

In today’s fast-paced business environment, lease accounting has become an increasingly complex task for organizations. Manual processes and outdated tools like Excel not only pose a high risk of errors…

The management letter from auditors, typically received by CFOs after the annual audit, highlights key financial findings and suggests improvements for internal controls. It also informs about new accounting standards…

Carbon accounting and sustainability management solution recognized for empowering Enterprises with the data and visibility needed to progress toward their ESG goals Woodbridge, N.J. –February 8, 2024 – Visual Lease…

Artificial intelligence has been at the top of people’s minds for all of the past year, and the accounting profession is no exception…

Leases are contracts in which the property owner allows another party to use the property or asset in exchange for some consideration, usually for money or other assets. This is…

Lease optimization software provider redefines excellence with a single system of record for lease accounting, management and sustainability tracking Woodbridge, N.J. – January 18, 2024 – Visual Lease (VL), the…

We’re excited to share the thoughts of fintech CEOs and industry leaders from across the globe to 2023’s key takeaways and what we should expect to be top of the…

Technology developers who serve the accounting profession have planned a bevy of new products, features, capacities, integrations, partnerships, initiatives and other major developments for 2024 that are all aimed at…

Solution provider is recognized for empowering companies to leverage their lease portfolios for strategic financial and operational outcomes Woodbridge, N.J. – Dec. 21, 2023 – Visual Lease (VL), the #1…

It’s that time of year again for the annual EKMH Innovators’ predictions! As the saying goes, the past is prologue: click and read past predictions about 2017 marketplace lending, 2018…

Is Excel good for lease accounting? 1. Lease terms constantly change, and it’s hard to keep up 2. Lease accounting calculations are complex and time consuming 3. Excel spreadsheets are…

3 Reasons to Stop Relying on Excel Spreadsheets 1. Leases are constantly changing 2. Excel can lead to non-compliance with accounting standards 3. The Office of Finance has evolved 3…

What is completeness assertion in lease accounting? Auditing completeness under ASC 842 What is audited under completeness assertion? How to ensure accurate completeness assertions Getting started with lease compliance Inaccurate…

The pressure to establish an ESG reporting framework is mounting as various regulatory bodies issue guidance.

Climate-related disclosure efforts are amplifying year over year (YOY), despite persistent and persnickety pain points, as more organizations widen the scope of the “discovery phase” of their environmental, social, and…

Building strategic financial partnerships has become a crucial factor for a company’s success and growth. Collaborating with the right financial partners can provide businesses with the necessary capital, expertise and…

Heightened scrutiny around environmental, social and governance issues is impacting a company’s operations on every front, including its lease management, according to a study from Visual Lease.

Companies are bracing for the Securities and Exchange Commission’s climate-related disclosure rule, according to a new survey.

Using ASC 842 Excel Templates How to Create Customized ASC 842 Excel Templates Best Practices for Data Entry and Formula Setup Best Practices for Document Organization Common Challenges with ASC…

Table of Contents What is a lessee? What is a lessor? Who is the lessor and lessee in a contract? Benefits for a Lessor vs Lessee How to approach accounting…

Survey reveals 84% of enterprise organizations are prioritizing lease management due to lease accounting standards and emerging regulatory requirements around environmental impact reporting Woodbridge, N.J. – Oct. 31, 2023 –…

Table of Contents How to Calculate the Present Value of Lease Payments in Excel Step 1: Organize Data Step 2: Use the PV Function Step 3: Repeat as Needed Cons…

Lease accounting and management have evolved into intricate processes, posing fresh challenges for financial leaders. From grappling with an accountant shortage to seeking enhanced lease flexibility during economic uncertainty and…

Controllers Council recently held a panel discussion on ESG 101: Practical Approaches for Navigating Compliance, Controls, and Sustainability Reporting, sponsored by Visual Lease.

Lease management is more complicated than ever before. Tenants and landlords are navigating a lot of hurdles, including organizations’ need for greater flexibility – according to the Visual Lease Data…

Longstanding pioneer in lease management and accounting continues to advance its platform capabilities to address evolving environmental reporting requirements Woodbridge, NJ – October 16, 2023 — Visual Lease (VL), the…

In the last few years, environmental, social and governance (ESG) planning has become ubiquitous. No matter the industry or company size, businesses have made tremendous investments to advance ESG policies—and…

California has taken a significant step toward addressing climate change by enacting the ground-breaking California Climate Accountability Package. This legislation not only sets the stage for comprehensive reporting of carbon…

In the world of commercial real estate leasing, Common Area Maintenance (CAM) charges play a pivotal role, impacting both landlords and tenants. CAM rent, often referred to as CAM fees,…

As a landlord, one of the most critical aspects of your rental property business is the lease agreement. A well-crafted lease agreement not only protects your interests but also provides…

Much like their for-profit counterparts, nonprofits must also follow specific financial reporting standards, including Accounting Standards Codification (ASC) 842. This blog post will delve into the essential aspects of ASC…

Woodbridge, NJ – September 27, 2023 — Visual Lease (VL), the #1 lease optimization software provider, today announced the winners of its annual Customer Excellence Awards, recognizing organizations that are…

Woodbridge, NJ – September 19, 2023 — Visual Lease (VL), the #1 lease optimization software provider, today announced the company’s newest offering, VL ESG Steward™, has been recognized by the Business…

When properly managed and prioritized, financial, operational and legal data has the potential to contribute significant strategic value to a business that extends far beyond meeting compliance requirements.

Getting clear insight into sustainability metrics means understanding your company’s real estate footprint

Leasing arrangements are a common aspect of business operations, allowing companies to secure assets and facilities without the commitment of ownership. However, within the realm of lease accounting, there’s a…

When it comes to managing leases and financial obligations, understanding how to calculate a lease amortization schedule is crucial. This schedule not only helps you keep track of payment timing…

In the realm of business decisions, the choice between leasing and buying assets has significant financial implications. To help evaluate these options, the concept of “Net Advantage to Leasing” comes…

When it comes to real estate and leasing agreements, terms can sometimes get a bit muddled. One such pair of terms that often find themselves used interchangeably are “lessee” and…

Company’s proven SaaS solutions are recognized in first analyst report dedicated to full lease portfolio management Woodbridge, NJ – August 29, 2023 — Visual Lease (VL), the #1 lease optimization…

Leasing is a common practice in business, allowing companies to acquire assets without a hefty upfront cost. However, situations arise where a lessee wants to transition from leasing to outright…

As a company navigating the intricacies of lease accounting, you’re no stranger to the importance of maintaining accuracy and compliance. Part of this process involves undergoing lease audits, a task…

The realm of commercial leases encompasses a complex lifecycle that spans far beyond the mere agreement itself. While it’s a subject that often invites surface-level discussions, grasping the full scope…

Navigating the world of lease accounting can sometimes feel like deciphering a complex code. The terms, regulations, and methodologies can leave even the savviest professionals scratching their heads. One such…

Navigating the Transition: Understanding Challenges Faced by Newly Public Companies and Strategies for Success In the dynamic landscape of public offerings, the surge in initial public offerings (IPOs) during 2020…

Company invests in its Partner network in preparation for the next stage of growth Woodbridge, NJ – August 8, 2023 — Visual Lease (VL), the #1 lease optimization software provider,…

The management and administration of leases is a complex challenge for organizations of any size, from a landlord renting out a room to a corporation renting out airplanes. With a…

In today’s fast-paced business landscape, small and mid-sized businesses (SMBs) face numerous challenges in managing their financial operations efficiently. As a business owner, you may be wondering “Do I need…

In the world of leasing agreements, there can be some confusion when it comes to the terminology used by attorneys and accountants. One such term is the “lease commencement date.”…

Contract management plays a crucial role in modern business operations, ensuring effective collaboration, risk mitigation, and regulatory compliance. With the growing importance of environmental, social, and governance (ESG) considerations, contract…

VL experts break down the recently announced sustainability reporting standards from the International Sustainability Standards Board (ISSB) The first-ever set of standards recently unveiled by the International Sustainability Standards Board…

Dedicated investments in its solutions, services and leadership expand company value Woodbridge, NJ – July 13, 2023— Visual Lease, the #1 lease optimization software provider, today announced its results from…

Joe Fitzgerald is Senior Vice President of Lease Management Strategy at Visual Lease. Over the past three years, environmental, social and governance adoption has become more ubiquitous, sweeping across industries.

Lease incentives play a crucial role in lease agreements, representing payments made by the lessor either to the lessee or on behalf of the lessee. These incentives are an integral…

As businesses increasingly recognize the importance of environmental, social, and governance (ESG) factors, the concept of ESG accounting has gained prominence. This blog post aims to shed light on ESG…

Taxfyle releases generative AI tax prep bot; Carbon accounting firm Greenly launches app store; and other accounting tech news.

In recent times, the importance of sustainability in financial reporting has gained significant traction. To address this growing need, the newly formed International Sustainability Standards Board (ISSB) has released two…

Cboe Global Markets, Salvatore Ferragamo, Bolt, MarketWise, GoGuardian, Visual Lease, InnovAge, MiMedx Group, MedMen

In today’s ever-evolving world, Environmental, Social, and Governance (ESG) has emerged as the ultimate framework for evaluating sustainability and ethical impact.

In today’s world, where environmental sustainability is a top priority, understanding carbon accounting has become crucial for businesses. But what exactly is carbon accounting? This article dives deep into the…

When it comes to commercial leases, there are various types and terms that can be confusing for both lessors and lessees. Among these terms are “triple net leases,” “pass-through leases,”…

Company continues to demonstrate its commitment to strategic growth and operational excellence Woodbridge, NJ – July 6, 2023 — Visual Lease, the #1 lease optimization software provider, today announced the…

Carbon accounting, sustainability management and ESG reporting tool receives global recognition on the heels of newly announced international sustainability standards (IFRS S1 and IFRS S2) Woodbridge, NJ – July 5,…

In the realm of financial management, companies are faced with critical decisions regarding capital budgeting. These decisions involve allocating funds to various investment opportunities. Additionally, companies often seek the assurance…

Lease purchase options provide companies with the opportunity to convert a lease into a fixed asset. These options allow lessees to exercise their right to purchase the leased asset during…

In the realm of financial accounting, fixed asset accounting holds significant importance for companies. It involves the meticulous tracking and management of owned assets, ensuring their existence, location, and allocation…

What is Prepaid Rent? Prepaid rent refers to lease payments made in advance for a future period. It represents an asset on the company’s balance sheet, as the prepayment can…

Leasing an asset with the intention to eventually purchase it is a common practice among businesses. Whether it’s an optional purchase at the end of the lease or a bargain…

Update: On June 26, 2023, The International Sustainability Standards Board (ISSB) announced their first two global sustainability-related disclosure standards in response to widespread demand for better transparency, consistency and reliability…

Table of contents: What is a finance lease? What is an operating lease? Key Characteristics of an Operating Lease Finance Leases vs. Operating Leases Understanding finance leases and operating leases…

Table of Contents What is Off-Balance Sheet Financing? ASC 842 Impact on Reporting Leases Importance of On-Balance Sheet Reporting Legal Regulations: The SEC’s Strict Stance Off-balance sheet financing refers to…

From Compliance to Optimization: Harnessing Lease Controls for Business Success Lease accounting standards implemented over the last few years (ASC 842, IFRS 16, GASB 87) require all organizations, whether they…

Chief financial officers are playing an important role in helping businesses navigate corporate ESG issues. We explore three key area

Finance chiefs should focus on three areas when building climate-reporting systems—collecting data, tracking regulation and coordinating with ESG raters

The regtech space is in for a major shake-up, with the FCA‘s new Consumer Duty regulations coming into effect in two months. This presents an opportunity for financial institutions to adopt…

Fixed Asset Accounting: Managing Assets and Leasehold Improvements In the realm of financial accounting, fixed asset accounting holds significant importance for companies. It involves the meticulous tracking and management of…

ESG and the Future of Real Estate: How Sustainability is Changing the Industry The real estate industry is undergoing a significant transformation as sustainability becomes a top priority for investors…

Related Party Leases under ASC 842 Recently, the Financial Accounting Standards Board (FASB) introduced new rules and clarifications regarding the treatment of related party leases under ASC 842. Although these…

GAAP vs. Tax Accounting: Navigating the Complexities of Financial Reporting With the introduction of ASC 842, some private companies are struggling with the requirement to record the vast majority of…

Table of Contents What is Accrued Rent? What is Deferred Rent? Accrued Rent vs. Deferred Rent: What’s the difference? Accrued Rent Example Deferred Rent Example Key Considerations for Rent Accounting…

“Why Lease Management Shouldn’t Be Ignored: The High Cost of Underestimating Your Lease Portfolio and How to Optimize It for Your Business Needs” Many companies are underestimating the total cost…

The ongoing effects of the pandemic, evolving workplace trends and unique economic circumstances have driven businesses to reconsider how and why they enter into new leases. But how exactly are…

This is part II of our Mastering Lease Accounting Compliance series. If you missed part I, you can read it here. Adopting a lease accounting standard can have a significant…

This is part I of our Mastering Lease Accounting Compliance series. If you’re looking for part II, you can read it here. Lease accounting standards such as ASC842 and IFRS16…

Company’s innovative solutions and customer-centric approach drive accelerated growth Woodbridge, NJ – April 19, 2023 — Visual Lease, the #1 lease optimization software provider, today announced its results from Q1…

Asuccessful CMO has many roles, including leading an organization’s marketing department, establishing marketing strategies, and tracking successes and failures.

When it comes to adopting the new ASC 842 lease accounting standards, initial implementation — as difficult as it may be — is only the first step in a long…

Visual Lease, a vendor of lease optimization software, announced VL ESG Steward, “a solution designed to track and report on the environmental impact of an organization’s owned and leased asset…

Lease software provider Visual Lease announced it has launched a new product, VL ESG Steward, designed to help organizations track and report on the environmental impact of their owned and…

Visual Lease launches ESG solution; GBS Tax and Bookkeeping rebrands as Cleer Tax and Bookkeeping; the ITA is looking for new president; and other news…

With more and more organizations focusing on ESG initiatives, we’ll use this blog to demystify what ESG is, why organizations choose to focus efforts on ESG related initiatives, and how…

The first sustainability-focused lease tracking and reporting software designed to help companies meet their environmental policy goals Woodbridge, N.J. – March 29, 2023 — Visual Lease, the #1 lease optimization…

U.S. businesses are looking to add office space this year, but their planning is more short-term than it used to be, according to a new survey by software specialist Visual…

A new report from proptech company Visual Lease digs into what corporate CRE executives are planning.

A study released this week by lease accounting software company Visual Lease found that 70% of the senior real estate executives polled say their clients are looking for more office…

The report also found more than half (52%) of senior real estate executives report that their companies are planning to add new satellite locations and 28% are looking to downsize…

Most firms still plan to grow their real estate footprints in 2023 despite the looming threat of an economic recession, according to a report from lease software provider Visual Lease…

For the last decade, the role of corporate finance professionals has increasingly expanded.

88% of businesses are planning for physical space needs just one year or less in advance Woodbridge, N.J. – February 22,2023 — Visual Lease, the #1 lease optimization software provider,…

In response to lease accounting standards, your business may have already set in place certain lease accounting systems and technology to achieve compliance. But did you know these solutions can…

Company achieves its fifth consecutive year of double-digit annual recurring revenue and customer growth Woodbridge, NJ – January 19, 2023 — Visual Lease, the #1 lease optimization software provider,…

A leading global automotive supply manufacturer manages its global lease portfolio and financial controls framework with the help of Visual Lease.

Lease optimization solutions provider Visual Lease has promoted Amie Durr to chief product officer; she will be the company’s first CPO. … AbacusNext, a software solutions provider specializing in the…

Today, many organizations lack control over their leases, which increases the risk of making costly errors, such as overpaying or missing a date for termination or renewal. (90% of senior…

Company continues to strengthen senior leadership team and invest in product innovation Woodbridge, NJ – January 9, 2023 — Visual Lease, the #1 lease optimization software provider, today announced its…

Accounting teams are often left scrambling to find lease information needed to wrap up the year and prepare for their audit. As businesses approach year-end, how can they ensure an…

What is depreciation in accounting? The 4 depreciation methods in accounting Can you change depreciation methods from year to year? Straight line method Declining balance method Units of production depreciation…

When considering the financial impact of your lease portfolio, there are five questions to keep in mind. Detailed below, answering these questions can help you better understand: Your readiness for…

Organization continues to invest in its leadership team to drive its next stage of growth Woodbridge, N.J. – November 1, 2022 — Visual Lease, the #1 lease optimization software provider,…

Company welcomes Visual Lease customers and partners to two-day event to network, discuss the future of lease accounting and recognize award-winning accounts Woodbridge, NJ – October 28, 2022 — Visual…

Leading technology provider joins forces with top accounting advisors to help companies master their lease administration and accounting software implementation Woodbridge, N.J. – October 27, 2022 — Visual Lease, a…

The $5 billion real estate company deals with a decentralized structure makes compliance and data tracking easy through Visual Lease.

Leading provider of lease accounting, administration and optimization software continues to make strategic investments to elevate its technology, services and team Woodbridge, NJ – October 13, 2022 — Visual Lease,…

Do your lease footnote disclosures comply with the new lease accounting standards? The footnotes of your financial statements must include certain information from your lease contracts. And with the newly…

Alexandra Betesh to amplify the voice of the customer in the company’s solutions, services and strategic partnerships Woodbridge, NJ – October 5, 2022 — Visual Lease, the #1 lease optimization…

Organization included on The Inc. 5000 List for third consecutive year, also receiving a 2022 PropTech Breakthrough Award, 2022 SaaS Award and 2022 Stevie Award for Employer of the Year…

New CEO makes first strategic hire to empower organization to further expand its offerings Woodbridge, N.J. – August 8, 2022 — Visual Lease, the #1 lease optimization software provider, today…

Founder and current CEO, Marc Betesh, transitions to Executive Chairman as company continues to expand and evolve Woodbridge, NJ – August 1, 2022 — Visual Lease, the #1 lease optimization…

Private companies and government entities continue to face challenges around properly managing and reporting their leases in accordance with the new lease accounting standards Woodbridge, N.J. – July 25, 2022…

The only software provider recognized as a Leader by G2 in Lease Administration and Lease Accounting continues to achieve double-digit annual recurring revenue, customer and employee growth YoY Woodbridge, NJ…

Have you ever wondered how the public can participate in the development of accounting standards? Do you have opinions you would like to share? Many accounting standards governing bodies, such…

Do you know where all your leases are? If you don’t, chances are you haven’t conducted a lease inventory for your business. Conducting a lease inventory is a standard practice…

Technical accounting expert from leading independent audit, tax and advisory firm will join the VL team to share exclusive insights on lease accounting compliance Woodbridge, NJ – June 14, 2022…

Fin-tech veteran to oversee strategic business operations at the leading lease accounting and management solution provider Woodbridge, NJ – June 1, 2022 — Visual Lease, the #1 lease optimization software…

On-demand webinar summary Lease accounting is an incredibly time-consuming, complex endeavor that involves a lot of initial preparation, cross-departmental collaboration and ongoing maintenance. So, how can businesses ensure their lease…

On-demand webinar summary Do you know if you are overpaying for your leases? Unfortunately, many businesses are, but are not aware of it until after they begin tracking their lease…

The new lease accounting standards have radically changed the way private and public companies record leases on the balance sheet. Naturally, this had a direct impact on lessees, lessors and…

On-demand webinar summary According to a recent VLDI survey, 35% of private companies were less than halfway through or had not yet started the process of gathering information needed to…

Company achieves double-digit YoY annual recurring revenue, customer and employee growth Woodbridge, NJ – April 18, 2022 — Visual Lease, the #1 lease optimization software provider, today announced results from…

Industry leader continues to host virtual events to help companies master lease accounting compliance Woodbridge, NJ – April 12, 2022 —Visual Lease, the #1 lease optimization software provider, announced its…

What is IFRS 16? What changed under IFRS 16? What is considered a lease under IFRS 16? Exceptions to the IFRS 16 Lease Accounting Standard IFRS 16 Impact on Financial…

When discussing commercial real estate, you’ll often hear about build-to-suit (BTS) leases, in which the landowner agrees to construct a property according to the requirements of the lessee, and the lessee…

The Financial Accounting Standards Board (FASB) recently issued an update to ASC 842 that addresses complexities associated with discount rate calculations. In this blog, we share how this update affects private…

Company achieves double-digit YoY annual recurring revenue and customer growth for fourth consecutive year Woodbridge, NJ – January 20, 2022 — Visual Lease, the #1 lease optimization software provider, today…

Industry leader to host a series of virtual events, sharing valuable insights to help companies master lease accounting compliance Woodbridge, NJ – January 11, 2022 —Visual Lease, the #1 lease optimization software…

Everything you need to know to make an informed decision when selecting lease accounting software for GASB compliance, so your organization can transition to the new requirements, stay compliant as…

Company continues to prepare for its next phase of growth Woodbridge, NJ – January 6, 2022 — Visual Lease, the #1 lease optimization software provider, today announced that Guy Zerega,…

What is lease capitalization? Lease capitalization is the act of recording Right-of-Use Assets and related lease obligations on a company’s balance sheet, as required for the lease accounting standard ASC…

One of the top independent lenders in the U.S. manages its ever-changing lease portfolio with Visual Lease, using data to make key decisions and helping to shave 80% of time…

Company sustains consistent double-digit growth over four years Woodbridge, NJ – November 18, 2021 — Visual Lease, the #1 lease optimization software provider, today announced that it ranked No. 264…

Company donates $25,000 to Habitat for Humanity International, The Affordable Housing Alliance and New Jersey Veterans Home at Menlo Park Woodbridge, NJ – November 17, 2021 — Visual Lease,…

Majority of surveyed tenants plan to expand their commercial real estate footprint in the New Year Woodbridge, NJ (Nov. 9, 2021) Visual Lease, the #1 lease optimization software provider, today unveiled a survey of 400 senior accounting and finance…

The majority of private companies have yet to implement the new lease accounting standard entirely, even though the effective date is fast approaching. Three-quarters (75%) of privately held companies surveyed this spring…

Leasing a commercial property is a huge step for a business. The right space in the right location can attract ideal customers and take an entrepreneur’s business to the next…

Company continues to strengthen its senior leadership team Woodbridge, NJ – October 26, 2021 — Visual Lease, the #1 lease optimization software provider, today announced that Erinn Tarpey, current Senior…

Partnership will empower organizations to accelerate their ability to comply with new lease accounting standards and maximize the value of their commercial real estate assets Woodbridge, NJ – October 13, 2021 — Visual Lease, the #1 lease optimization software provider, today announced a partnership…

Company now helps more than 800 organizations manage upwards of 500,000 leases Woodbridge, NJ – October 11, 2021 — Visual Lease, the #1 lease optimization software provider, today announced results…

Solution provider to host a series of virtual events, gathering industry experts to share unique insights and opportunities around lease accounting Woodbridge, NJ – Sept. 27, 2021 — Visual Lease,…

The decisions you make when purchasing lease accounting software have huge implications for your business.

Are you truly getting the most value out of your financial technology? We recently surveyed 500 senior and accounting finance professionals and found that 53% of respondents use three to…

Woodbridge, NJ – September 13, 2021 — Visual Lease, the #1 lease optimization software provider, has been named a Best Place to Work in New Jersey by NJBIZ. The organization was recognized for its unique company culture, strong leadership, high levels of…

Lease accounting compliance is not just a one-and-done disclosure. It is a new approach to accounting that includes an ongoing, cross-departmental effort – and a much higher level of scrutiny….

Under the FASB ASC 842 standard for lease accounting, organizations face significant changes including both new disclosures and specific requirements for how to report those disclosures. For instance, in the…

The upcoming FASB accounting changes are not only a challenge for corporate accounting teams, but also for the commercial real estate group. To get you up to speed, here’s an…

Table of Contents What is Capital Lease Accounting? What is a Capital Lease? Main Differences Between a Capital Lease vs. Operating Lease What are the 4 Criteria for a Capital…

Public companies have significantly changed their financial processes in the past year and are not done yet, according to data released last month by Deloitte.

Woodbridge, NJ – August 30, 2021 — Visual Lease, the #1 lease optimization software provider, has been named the winner of a Gold Stevie® Award in the Employer of the…

Last year, the Governmental Accounting Standards Board (GASB) voted to defer the effective date of lease accounting standard GASB 87 to give public sector entities more time to adapt to…

Private companies are facing a deadline on implementing the new lease accounting standard, but recent updates in the rules could make an impact on their financial statements and disclosures.

Organization recognized as one of the fastest-growing private companies in America for the second consecutive year Woodbridge, NJ – August 17, 2021 — Visual Lease, the #1 lease optimization software…

Newmark delivers an array of strategic brokerage services to its broad client base, including owners, occupiers, investors and founders. See how they use Visual Lease to manage their lease portfolio here.

Visual Lease, the #1 lease optimization software provider, today unveiled the results of an in-depth study of 500 senior finance and accounting professionals analyzing where companies are in their efforts…

Visual Lease unveiled the results of an in-depth study of 500 senior finance and accounting professionals analyzing where companies are in their efforts toward achieving compliance with ASC 842. The report…

Package provides robust tech capabilities and all-inclusive implementation and support required to achieve lease accounting compliance with ASC 842 Woodbridge, NJ – August 10, 2021 — Visual Lease, the #1 lease…

While 100% of surveyed companies agree on the business value of complying with the lease accounting standard, most are underconfident and unprepared for the looming deadline Woodbridge, NJ (July 29,…

Company reports key strategic investments and double-digit annual recurring revenue growth year-over-year Woodbridge, NJ – July 20, 2021 — Visual Lease, provider of the #1 lease optimization software, today announced results from…

In a 2020 IDC survey, 42% of technology decision makers reported that their organizations planned to invest in technology to close the digital transformation gap. We expect that number has…

There is power within your lease portfolio. Over the last year, public and private businesses have taken a closer look at their leases – and experienced the downstream benefits of…

Last year, the Financial Accounting Standards Board (FASB) provided private companies with an extra year to adopt lease accounting standard ASC 842. When this was announced, 63.8% of surveyed private company executives…

Real estate leases can serve as key strategic assets for companies, presenting opportunities to improve the execution of a business strategy while also creating operational efficiencies. But leases also present…

This article originally appeared here in Forbes. As a result of Covid-19 and the changing landscape related to leases, private companies have received more time to prepare for and adopt…

The Governmental Accounting Standards Board released updated implementation guidance for its leases standard, which is going into effect soon, along with other accounting standards for state and local governments.

This article originally appeared here in Forbes. In 2020, many companies were forced to make tough decisions regarding their leased commercial spaces. From office closures to consolidations and deferrals, many…

In response to the ongoing effects of Covid-19, businesses across all industries have had to adjust not only their strategies and goals but also their workflow and styles to remain…

Lease accounting is a massive, cross-functional effort. It involves various stakeholders and systems that impact (and are impacted by) leases. It is not just an accounting problem – and goes…

For companies that are reporting on a calendar year and have completed their audit, CFOs have recently received or will shortly receive a management letter from their auditors. The management…

Lease accounting (ASC 842, IFRS 16 or GASB 87) is not your average one-and-done disclosure. This whole new approach to accounting requires you to account for lease changes throughout the year with a higher level of scrutiny. A…

It’s been just over a year since the U.S. experienced a series of lockdowns in response to the Covid-19 pandemic. Lessees and lessors have had to quickly adjust their strategies to…

Landlords and tenants are struggling to reconcile 2020 building operating expenses and service charges in an atmosphere of highly irregular occupancy and operational adjustments.

With the ASC 842 deadline for private companies looming, there are several things private organizations can do to set themselves up for success.

Real estate, as an industry, has been more accepting of technology’s benefits to the trade in recent years. A growing number of real estate companies and professionals have embraced tech…

Among the many different calculations used in lease accounting, the incremental borrowing rate may be one of the most misunderstood. The incremental borrowing rate (IBR) is the interest rate a lessee would…

Commercial real estate overhead has never faced more scrutiny. While today’s highly agile workforce brings with it a newfound level of productivity, there are various impacts and considerations felt across…

These are the considerations that financial professionals should keep in mind to ensure they are prepared for changes that may emerge due to COVID-19.

To survive and thrive in today’s new norm, these same companies now need to evaluate how these decisions will continue to affect the leasing landscape, and what that means for…

Table of Contents What is a lease term? Lease lengths defined under ASC 842 Long-term leases under ASC 842 Short-term leases under ASC 842 Month-to-month leases under ASC 842 ASC…

This past year, organizations across the globe have faced unprecedented challenges as they navigate new business models and virtual work environments. For many, it’s been a race against the clock…

Another day, another breathless survey repeating what we’ve been hearing for the last year: work-from-home is more than just a passing trend, and it just may be here to stay….

What are rent concessions? Rent concessions are discounts, incentives, or other benefits provided by landlords to tenants. Landlords sometimes offer rent concessions to entice tenants to sign a new…

Commercial office leases were on the chopping block last year as companies grappled with the impacts of COVID. Of the companies surveyed in a new Visual Lease report, 50% received…

Changes in accounting standards have made lease accounting more difficult. Adopting IFRS 16 lease accounting, for example, has made compliance cumbersome as it involves adjusting to new policies, systems and…

Beginning in 2006, there was a concerted effort by the two accounting standard bodies (FASB and IASB) to synchronize their respective standards on leasing to assure consistency and uniformity. The…

How has COVID-19 impacted the road to compliance and the accounting industry? Visual Lease’s Joe Fitzgerald discusses why FASB has proposed new changes to its lease guidelines and what it…

Table of Contents What is a roll-forward report? The importance of roll-forward reports Roll-Forward Reports: Meeting Lease Accounting Standards The advantages of roll-forward reports Creating Comprehensive Roll-Forward Reports Why…

Lease portfolios often account for a massive portion of a company’s risk exposure and overhead. And yet, most businesses lack visibility into their leases to understand their obligations and options – and…

As the accounting profession navigates the challenges brought on by COVID-19, FASB shifted the deadline to grant private companies more breathing room to achieve compliance with its major lease accounting…

How to Abstract, Manage and Report on Lease Data When FASB issued its update to the lease accounting standard, the main goal was to increase the transparency and comparability of financial reporting. …

In the current economic environment, businesses are searching for new ways to save cash. However, they often overlook one critical aspect of their business: real estate management. Real estate leasing…

In the current economic environment, businesses are searching for new ways to save cash. However, they often overlook one critical aspect of their business: real estate management. Real estate leasing…

Hundreds of private organizations have begun their journey towards lease accounting compliance. Although, many of them underestimate the amount of effort involved with preparation. In particular, assembling a team…

As COVID-19 has wreaked havoc on the CRE industry, many tenants have been forced to make tough decisions when it comes to commercial real estate leases. Marc Betesh, founder and…

The Financial Accounting Standards Board (FASB) has issued a proposed Accounting Standards Update (ASU) intended to improve three areas of the leases guidance.

Buying technology for cross-functional teams can be notoriously nightmarish, especially as you dive in and realize you need to expand your scope, shorten your timelines, or overhaul your processes along…

Following the FASB’s recent decision to extend the deadline for its ASC 842 standard for a second time, privately held companies have an additional 12 months to prepare to comply…

Since the start of the Covid-19 outbreak, commercial tenants have fallen behind on rent payments as cities across the U.S. have been on full or partial lockdown for months on…

How to Save Money and Improve ROI with Lease Accounting Technology Leases are complex documents that can be challenging to interpret. Critically important details are often buried deep within a…

Lease Accounting Compliance: Lessons from Public Companies Although private companies still have some time to adopt the new lease accounting standards, public companies have already had to meet their compliance…

Office Lease Transparency Is More Important Than Ever: A Q+A With Marc Betesh, CEO and Founder of Visual Lease about where he thinks the office lease market is heading.

Visual Lease recently surveyed tenants to see how they have been impacted, any payments they withheld or concessions they have been offered, and how the pandemic is impacting their future…

Fall and winter will bring more lawsuits and evictions, industry sources say. CEO of Visual Lease, Marc Betesh, comments.

Visual Lease, a lease accounting and management solutions provider, has appointed Amy Land as Director of Human Resources.

Marc Betesh interviewed with Akiko Morris at The Real Deal around TikTok’s lease and the growing work from home trend.

What Contractors Don’t Know About Equipment Leases Could Cost Them a Fortune. Marc Betesh, Visual Lease CEO and Founder gives his insights and tips on what you should know about…

NJ-based company, Visual Lease, made the list of one of Inc. 5000’s fastest-growing companies.

Many private companies breathed a sigh of relief when the deadline for transitioning to FASB’s newest lease accounting standard was once again extended — this time, until 2022. But make…

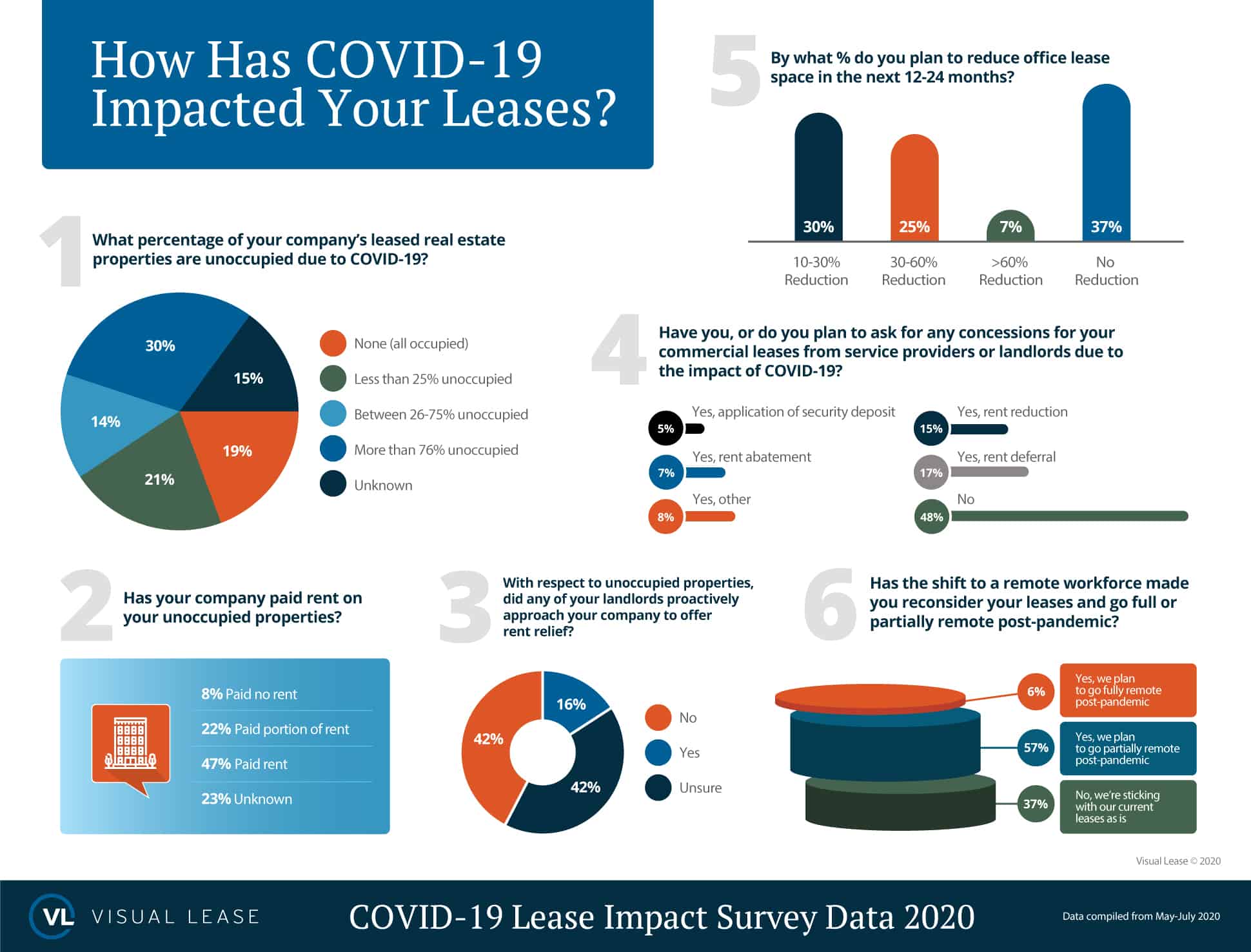

We recently surveyed hundreds of companies, including 700 Visual Lease customers (see Fig. 2), about the impact COVID-19 has had on their corporate real estate leases. As seen in the…

There is no excerpt because this is a protected post.

A large number of companies have failed to make rent payments on their unoccupied commercial properties as ongoing COVID-19 shelter-in-place orders have shuttered operations.

The legislation “significantly impacts the validity of existing contracts,” quoted Marc Betesh. “It would completely undermine the real estate industry and the economy. If you can’t rely on the validity…

With all the business closures and cutbacks due to the COVID-19 pandemic, a lot of companies are worried about not only managing their lease expenses now, but also accounting for…

Visual Lease supports the local town of Woodbridge, NJ with donations to support essential workers during COVID-19.

Restaurants and retailers are seeking rent concessions this spring to ease cash flow as stay-at-home orders slammed their businesses.

While the deadline for FASB lease accounting compliance will likely be pushed back, now is certainly not the time for your clients to press pause on getting a handle on…

Almost half of New York renters said they will struggle to make today’s rent payment.

How is #COVID19 impacting commercial lease agreements? Visual Lease CEO Marc Betesh joins Jill Malandrino on Nasdaq #TradeTalks to discuss how businesses are being impacted by the coronavirus the move…

In an act of relief for companies during the coronavirus pandemic, the Financial Accounting Standards Board (FASB) recently voted to propose a one-year deferral of major accounting standards, including ASC…

With ever changing needs to lease agreements as the pandemic unfolds, real estate stakeholders are calling for technology that provides quick access to documents for modification.

The entire commercial real estate sector will be affected, and the uncertainty hits tenants and landlords alike. Can I afford to keep paying rent?

It’s crucial to properly manage lease documentation to avoid serious financial risks, such as overpayment or missed renewal dates. Furthermore, proper lease management has become more critical than ever due…

Visual Lease is committed to the health and safety of our employees and the community, as well as to providing your organization with the highest levels of uninterrupted service and…

Visual Lease, the leader in lease accounting and management software, today announced it has been selected as a 2020 “Best Place to Work in New Jersey”. The annual NJBiz “Best…

Leasing vs buying is not an easy decision to make regardless of the asset involved. While there are lease vs buy analysis Excel sheets, choosing one over the other is…

With all the new lease accounting rules you have to contend with — whether you follow ASC 842, IFRS 16, or GASB 87 — the prospect of generating lease accounting…

As of the beginning of this year, GASB 87 lease changes have gone into effect. These new lease accounting rules have a substantial impact on government entities and public institutions…

There have been several major changes in the way businesses address service contracts in recent years given the new standards and updates on the existing standards. For one, the new…

If you have signed an operating lease for space, built leasehold improvements, and determined that you are legally required to take out the leasehold improvement when the lease expires, then…

The Financial Accounting Standards Board (FASB) and International Accounting Standards Board (IASB) are not blind to the tedious task facing firms once the new standards take effect. Hence, the creation…

How often do you have this experience when evaluating enterprise software? The vendor gives a demonstration of an amazing solution, walking you through complex tools that do exactly what you…

In attempt to become compliant with the new lease accounting standards, particularly ASC 842 and IFRS 16, there are many intricate details that accountants often have questions about. Today we’ll…

Looking to select the best software for the new lease accounting standards? Due to the tight compliance timelines and complex lease information, this decision can be a difficult one to conquer….

When companies think about purchasing lease accounting and lease administration software, many make the mistake of considering these tools as a cost of doing business. The mistake is understandable, because…

The Financial Accounting Standards Board (FASB) approved its August 2019 proposal to grant private companies, not-for-profit organizations, and certain small public companies various effective date delays on its credit losses…

CFOs of private companies don’t have much time to comply with new lease accounting standards even if FASB extends the start date a year, as it has proposed.

As the standard for lease accounting software, Visual Lease provides the tools you need to achieve compliance. We make it easy to track, report, and manage your lease finances within…

Woodbridge, NJ, July 16, 2019 – Visual Lease, a cloud-based lease management and accounting software provider, received a growth investment from Spectrum Equity, a leading growth equity firm investing in…

Marc joins ranks of unstoppable entrepreneurs in New Jersey region Woodbridge, NJ, May 6, 2019 – EY today announced that Marc Betesh, Founder and CEO of Visual Lease, is a…

Woodbridge Mayor John McCormac thanks Visual Lease CEO Marc Betesh for generous contribution to “Have-A-Heart” food drive. Have-A-Heart supplies Woodbridge food pantries with food donated from local business, schools and…

Visual Lease, a New Jersey-based lease management and accounting SaaS company, today announced Clark Convery joined its team as Chief Operating Officer. Prior to Visual Lease, Convery was General Manager of the Enterprise…

For public companies who must comply with FASB ASC 842 and/or IFRS 16 within a few short months, how to get ready FAST is the critical question. The fact is,…

An agile leased real estate portfolio supports an agile workforce Business agility is a paramount goal for today’s business enterprises. Given the rapid pace of change, and the shortening of…

Information technology is revolutionizing CRE Technology is transforming everything today and this is true for commercial real estate technology as well.

Lease modification accounting is a subject that isn’t getting as much attention as it should… yet. That’s going to change the closer we get closer to the deadline for IFRS…

Back in the 1980’s I was a manager in the corporate real estate department of Xerox Corporation. One of my assignments was to participate in a quality improvement program called…

Last month, Visual Lease joined Bloomberg to sponsor a black tie gala that raised over $130,000 for All Hands and Hearts — Smart Response, a non-profit organization that provides disaster…

The growth of co-working office spaces and flexible workplaces is explosive worldwide. In a recent article in CoreNet’s March 2018 issue of “Leader” magazine, the author reports that co-working has…

Over sixteen years ago while a Gartner analyst, I launched a series of research reports on the subject of virtual teaming. Because of mobile technology and the growth of telework,…

In my last couple of blog posts, I covered the basic elements of real estate market analysis and the real estate market cycle. In case you missed them: Real Estate…

In my last blog post, I covered the basic elements of real estate market analysis. In case you missed it: Real Estate Market Analysis: A Primer for CRE Executives In…

What CRE can learn from a real estate market analysis report Virtually all real estate service firms offer some type of real estate market analysis. These reports are typically offered…

Organizational Challenges & the New Lease Accounting Standards There are many organizational models that are used to manage corporate real estate. Companies adopt primarily two models: centralized and decentralized. In…

What is beacon technology? There’s been increasing interest in what is known as beacon technology. Usually associated with retail marketing, beacon technology first emerged in 2013. Today the technology is…

There’s been a growing buzz throughout the tech world about blockchain technology and its associated topic of Bitcoin, the blockchain enabled digital currency. The specific characteristics of blockchain make it…

Deal bolsters cloud-based lease management and ASC 842 services CHICAGO — Grant Thornton LLP, the U.S. member firm of Grant Thornton International Ltd, has entered into a preferred vendor agreement…

Early in 2015, I reported on a dinner meeting of the Corporate Real Estate Leadership Counsel in San Francisco. I was a member of this group when I managed corporate…

The new FASB and IASB leasing standards go in effect in 2019. And one of the provisions requires a retrospective accounting of lease costs back to 2017. Recently PwC and…

We continue to get questions from our clients regarding the new leasing standards. Here are several of the more common questions with extended answers: Question #1 What are the new…

How do you organize your CRE department? The structure of the CRE organization should directly correspond to key processes such as leasing, construction, design and facilities management. Organizational structure varies by the size of the real estate portfolio, the type of industry, the level of outsourcing and the geographic dispersion of the real estate portfolio.

Perhaps one of the most critical aspects of corporate real estate management is the subject of process management and the software that supports it. Process management is a major subject in the topic of quality management. It has been a topic that has dominated management subjects for decades. Most software applications have specific functionality that addresses process management; particularly around work flow.

In the latest issue of the LEADER, the official publication of CoreNet, two of my former colleagues, Mike Joroff and Frank Becker, co-authored an article entitled, “Exploit Change and Uncertainty to Drive Corporate Value.” Becker and Joroff collaborated with me on several projects, including Office 88 (Becker-1983) and the Agile Workplace (Joroff- 2003) The authors make the case that many of the assumptions about the office, technology, and work need to be updated and revised to reflect the new trends visible in the global workplace.

In February, IBM announced that it is reversing its 10 year old policy that allowed telecommuting. All marketing employees must now report to six IBM offices or be terminated. The offices include New York, San Francisco, Austin, Cambridge, Atlanta, and Raleigh. Other employee groups will be affected over the next six months. Employees have 30 days to make their decision. The policy will also be implemented throughout Europe.

In 1972, when I first took on a real estate management job at Xerox in Chicago, one of my most important tools was my Rolodex. For the younger reader of this blog, I should explain that the Rolodex was a simple filing of business cards or small index cards, arranged in alphabetical order, and containing names, phone numbers, and mailing addresses of service firms, colleagues, and other contacts. I would use the Rolodex at least 2-3 times a day to look up service people who I might need in an assignment or project, or check in with contacts who might help as a reference.

In an earlier blog post I addressed the subject of outsourcing corporate real estate services. One of the key services that is central to the real estate process is the need for design services, typically interior design services. Maintaining a design team internally is expensive and unnecessary. For some organizations having a design professional as a member of the CRE staff is advisable for the purposes of supervising the design contract firm and evaluating designs in various stages of development.

In several of my blog postings over the last two years I made reference to the subject of outsourcing CRE functions. But my references were brief. So over the next several blog entries, I plan to delve deeply into the subject. My plan is to first discuss the general pros and cons of outsourcing while providing the rationale for outsourcing various CRE functions. I will then focus on three service areas: lease transaction services, design services, and property management services. I’ll also touch on other activities such as facility management and physical security.

Realcomm, the technology focused real estate web site, recently published an article entitled “The Data is Coming In: Corporate America is Using Less Than 50% of Its Real Estate.” This is no surprise; I remember from my own experience that our offices were nearly 30%-50% vacant at any one time.

One of my colleagues recently posed the question “Is there an example of a decision you made that you would do differently now based upon technologies available today?”

From time to time clients raise the question of the difference between corporate real estate and facilities management. In essence, they’re asking why we have two different professional designations since they both seem to have the same responsibilities. But the two professions have distinct differences and responsibilities. Here we explore these differences and attempt to bring clarity to the issue.

There’s always a dispute within the organization aboutthe issue of chargebacks, particularly facility occupancy costs. Department heads typically question the need for charging back occupancy costs, since they don ‘t feel they have any direct control over these overhead costs. But occupancy costs are directly linked to staffing, so it’s logical to burden a department with its share of occupancy costs relative to staffing levels. The argument for chargebacks centers on the need for reinforcing cost containment, as well as maintaining a level of fairness in the organization.

In March of this year, Sodexo released a study of the corporate real estate profession, focusing on its image and value as a viable career path. Having practiced in the profession for over twenty-five years, I experienced first hand the challenges and rewards of corporate real estate as a junior manager, a senior executive and as a broker and consultant . For many years, corporate real estate didn’t enjoy the cache or prestige of other corporate functions such as marketing, finance, and even Information Technology. But this is changing with the advent of new leasing standards and workplace strategies. So it was with this personal back ground I took a special interest in the Sodexo survey and report.

In June of this year, Corenet Global published a report entitled, “The Future of Corporate Real Estate.” The report covered several major trends which would influence the corporate real estate function. Such trends as sustainability, advanced information technology, globalization, the “gig economy”, urban development, workplace changes, etc. would all have a major impact of the future of corporate real estate.

In a recent article in the New York Times, the report described how corporate America is moving from suburban campuses back to urban markets, despite the higher cost of central business district office space.

Security and safety is now high in the minds of CRE managers, because of the eruption of violent terrorist attacks worldwide. It seems a day doesn’t go by when some violent outbreak takes the lives of multiple victims. In many companies the CRE executive is responsible for physical security and thus, must develop a plan for insuring the safety of people and assets in the workplace. Typically the IT department has responsibility for information security, but it’s wise for the CRE executive to coordinate with the CIO on security. So what are the key priorities that need to be addressed in a workplace security plan?

A key process for the CRE executive is overseeing the site selection process, particularly for major office, data center, or manufacturing sites. I’m going to focus on office site selection since this typically represents the most frequent type of leasing actions.

It’s been over a week since the British vote to exit the European Union, and the situation is worsening for property owners in the UK. The greatest impact is happening in the financial markets. Real estate Investment trusts (REITs) are experiencing increased redemption causing some of the biggest funds to halt outflows as a means to protect values for existing investors.

Earlier this week, the world was stunned by the British vote to leave the European Union within 2 years. The most likely impact on corporate real estate markets and operations will be immediate. While equity markets have recovered somewhat from the lows, it’s unlikely that the stock market will return to its historical highs of last week any time soon.

In the last several Blog posts, I’ve explored the various steps in becoming a CRE executive. Today I want to address the question of CRE organization. There is no one organizational model that is ideal. But there are various structures thatfit the needs of most business entities.

In our continuing series about how to become a CRE executive, the conversation would be incomplete without a brief review of the IT basics relating to CRE management.

Entering a career in Corporate Real Estate can take many paths. During my career I met countless CRE executives with myriad backgrounds. Some moved from real estate services such as brokerage or consulting. Others came into the profession as architects or engineers. A popular avenue is facility management, since the disciplines of property and maintenance management are a natural stepping stone to real estate management.

In this blog entry I would like to introduce the topic of CRE leadership and management. I hope to explore the topic over the next several weeks with the hope that these personal observations will be useful to those readers who aspire to make corporate real estate management a long term career.

Performance management in corporate real estate has matured rapidly over the last ten years due primarily to the evolution of sophisticated real estate management systems. With the advent of integrated workplace management systems(IWMS), and now cloud based point systems (like Visual Lease), CRE organizations have a wide range of options in the type and utility of portfolio management systems.

Space (square footage) is the universal unit in corporate real estate management. It defines the basis for rental, allocation of costs to different occupant groups, is the primary factor in developing space requirements for different utilizations such as offices, work stations, conference rooms, storage spaces, etc. Most companies develop a set of space standards as a means to design office layouts, allocate space to various functions, and use to forecast space demand over time.

Back in November of last year I cited a study by CBRE that seemed to debunk several myths about the Millennial generation and the office environment. The essence of the study was that while Millenials had certain preferences and attitudes about the workplace, in general there was little difference between the generations about their desire for workplace flexibility, preferences for urban settings, more collaboration, and more autonomy. However, in a recent article about Millenials in the March 15 issue of Fortune magazine, the theme of the article is about how to attract and retain the Millennial generation.

It was early summer of 1995, and I was aboard a French SST Concord traveling at roughly Mach3 from New York to Paris..

In my last Blog posting I covered the subject of co-working; an office concept which entails using office space on a shared basis. Unlike executive suite operations such as Regus serviced offices; co-working is less formal, collaborative and aimed at the millennial generation. Co-working is growing rapidly in most major urban areas, particularly in central business districts. The outlook for growth is stunning, with nearly 2000 locations anticipated within five years. One of the most successful operators, Wework, now has a market cap of over $5 billion, with no slowing in growth expected.

But co-working is not without its drawbacks.

The primary driver of this growth is the rise of the contingent worker, which represents about one third of the US workforce according to government estimates. With the advent of mobile technology and cloud computing, millennials, those between the ages of 20-35, seek non-traditional work environments as well as a sense of community. Co-working meets these needs by offering informal and edgy workplaces, and a spectrum of services that might include WiFi, marketing training, social events, and even conferences aimed at the young, independent entrepreneurs.

For some large companies, the charter of CRE has expanded to include physical security, sustainability, and now even the charter may include company wellness programs. In an open online survey conducted by CoreNet Global, a strong majority of respondents – 80 percent — said that corporate wellness initiatives represent a “significant trend,” while only 20 percent said that they were a “passing fad.”

Earlier last week I attended a dinner in San Francisco of a group of corporate real estate executives. During the evening I had a chance to speak with several of the attendees, and queried what were the major issues being discussed by the group at their 2 day meeting. A number of topics came up including the subject of Corporate Wellness, Sustainability, and Strategy.

A major question I am asked on occasion is what is the best way to organize the corporatereal estate function. There are several fundamental principles that should be considered to answer this question.

The long awaited new lease standard has arrived! The International Accounting Standards Board (IASB) released its version of the new lease standard last week with implementation scheduled for early 2019. The US accounting standards board (FASB) is expected to release its version shortly with implementation to follow soon after IASB’s.

During my tenure as head of real estate I always began the new year with a few resolutions that would become goals for the year ahead. These were typically above and beyond department objectives for the year and represented personal goals for some kind of improvement. Here are a few that I recall..

With the New Year it’s a good time to take stock of the corporate real estate domain and consider the challenges facing the managerial profession responsible for the corporation’s real estate assets and services in the year ahead. Here are five major challenges if dealt with effectively will determine in part the success of corporate real estate in 2016.

In the last several blog posts, I’ve explored various aspects about the future and how these trends may affect the workplace. One key variable in the future workplace is demographic differences, or how generational differences will impact workplace design. I suspect we all assume various truisms about the major generations.

In my last Blog entry I wrote that IOT would be a megatrend that would revolutionize building operations by imbedding machine addressable technology in every aspect of the built environment. IOT is not new. In fact the technology has been around since the late 1990s. Gartner estimates that there will be nearly 26 billion devices on the Internet of Things by 2020.

Price Waterhouse Coopers recently published a report, “The Future of Work, a Journey to 2022,” in which the consulting firm developed three scenarios of how the future of work may evolve over the next 7 years. Mike reviews them here.

October, 2015 is the month and year when Marty McFly traveled from July 1985 to the future in the famous Delorean time machine. Thus, it’s a good time to review past predictions of the changing workplace, and to rate their accuracy. Predictions of the future almost always miss the mark. Here are a few of my favorite classic misses:*

In a earlier white paper, The Lease Accounting Tsunami; Are You Prepared to Weather the Storm?, I wrote that users should evaluate the effects of the new FASB/IASB on a company’sdebt structure, debt to equity, and other factors that would be affected by the new standard, assuming lease liabilities would be considered as debt. In point of fact, the FASB explicitly decided that Type B lease liabilities should not be considered as “debt.” However, the IASB which treats all leases as Type A leases or capital leases, does consider these liabilities as “debt-like liabilities.” (Their exact words) As one of my accounting friends advised “The accounting for Type A leases requires IASB companies to record interest expense, and segregates payments on the lease liability into operations and financing outflows per the cashflow statement, which is consistent with debt.”

Thus, US companies will experience less impact from the new standard, particularly as it relates to debt covenants, debt to equity metrics, and capital structures. But US companies with significant international lease portfolios subject to the IASB standard, will see their debt levels increase.

Having split my career between facilities management and IT management, I gained an appreciation of how these two professional disciplines have many similarities, but distinct differences which createpolitical difficulties in many organizations.

Virtually the entire infrastructure of the enterprise combines traditional facilities assets: buildings, land, furnishings, and lease contracts and IT assets: servers, storage, networks, mainframes, and applications. In the last half century these distinct asset classes have become ever more intertwined, interdependent, and fused to create work platforms.

In this morning’s New York Times, it was reported that Goldman Sachs recently consolidated from three floors to two in its major Manhattan office tower. The Times reports that “the changes in real estate have helped Goldman reduce its cost by 17 percent since 2010.” This is yet another example of the value in corporate real estate strategic planning and why I wanted to spend a bit more time on the subject.

In the last blog entry we reviewed how the strategic planning process evolved from forming the planning team, benchmarking performance indicators, and setting priority objectives. Outlined below is what the strategic plan looks like:

So what are the major components of the corporate real estate strategic plan?

At the time I was the Corporate Real Estate Director of a major multinational corporation with a headquarters in New York City. It was the mid 1990s, and the real estate market in midtown Manhattan was a bit soft. Senior management wanted to move out of New York to an owned (and relatively vacant) office building in suburban Connecticut.

We are frequently asked why we need a new FASB lease standard.. here are our thoughts…

What are some guiding principles for selecting and investing in software functionality in support of your facilities and real estate operations?

Perhaps one of the most daunting and complex responsibilities of the corporate real estate executive is the management of lease escalation costs. These costs which represent expense pass- thrus from the landlord to the tenant can represent nearly half or more of the cost of tenant occupancy.

Many companies today use tenant representatives to handle various leasing actions such as leasehold relocations, renewals, expansions, and extensions. Tenant representatives are commercial brokers who typically operate exclusively as tenant advocates, while collecting commissions from building owners. This may seem like a conflict of interest, but the industry has self-regulating practices to avoid most abusive behavior.

There’s compelling logic to combine a lease audit service with a lease management system such as Visual Lease..

Advances in technology and changes in user behavior are driving significant transformation in Integrated Workplace Management Systems (IWMS) software architecture and delivery..

As a Gartner analyst some years ago, I focused on the real estate/ facilities management software space. I had spent nearly thirty years in corporate real estate, and was perhaps the only analyst at Gartner who had a broad and varied background in corporate real estate. I wrote one of my first research notes, in April of 2003 on the corporate real estate and facilities management space when I identified the key components of what I later named IWMS.. a lot has changed since then.